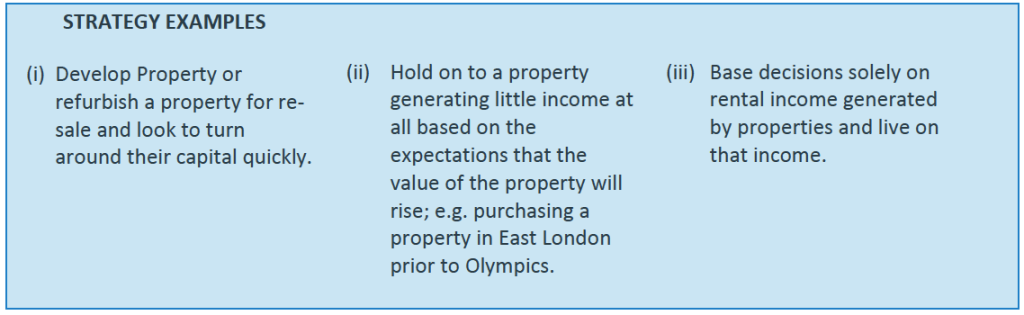

- In a Buy to Let sense this is where a landlord seeks to invest in property primarily to benefit from the increase in the value of the property.

Some examples of how this can be achieved include:

– Buying at the right time in the market cycle

– Buying in the right area

– Renovating a property

– Negotiating hard or buying cheaply

– Developing or converting a property

Income Examination

In the context of Buy to Let, this is where landlords seek to generate a positive cashflow from properties through achieving a regular flow of rent that is over and above expenditure.

This can be achieved through:

- Low cost financing techniques

- High occupancy

- Tenant charges

- Self Management

- Achieving maximum rent

Mixed Strategy

It’s obvious, earning from Capital AND Income is clearly the way to go, right? Adopting this technique can be risky as it can lose the focus that strategy is intended to provide.

A mixed strategy can best be applied to a portfolio, where some properties may be purchased for Capital Growth and others for Income. This minimises portfolio risk but typically this specific strategy would be applied to a property or group of properties.

(1) Pick the right strategy for you

The right strategy for your current position, your preferences, your knowledge and time, your aim, objectives and your means.

(2) There is no ‘Wrong Strategy’

Strategy is important to ensure your decisions are all pulling your investment in the right direction and are consistent.

(3) A Strategy Allows Other Benefits

A capital strategy may accrue income benefits and vice versa.

Why is Strategy Important?

A Buy to Let property or portfolio is a business and every business needs a strategy.

A Capital Investment business need not have a complicated strategy. A strategy allows the detail (‘Tactics’) to be adopted in a consistent manner in order to meet the strategic objectives. It also allows a true assessment of the performance of the business.

Example: Poor occupancy rates may not be a big issue in a capital appreciation strategy; conversely they are a big issue on an income strategy.

Timing of evaluations is also crucial. Income strategies should be reviewed regularly and frequently; capital strategies are for the longer term.

Maximising Your Strategy

Basic components that are critical to any strategy. Landlord Essentials!

Many tactics that you will employ will be dependent on your chosen strategy but come what may, all of the below topics need to be looked at in line with your strategic objectives.

(1) Property Section

Absolutely crucial so whilst most landlords think it too obvious to invest that much time on, it’s the cornerstone of any investment strategy.

Local Knowledge will be so important in this area but select your property with your strategy in mind, not based on any emotion or because you ‘like’ the property. Typically the ‘right’ properties will be sought after by more than one investor but just because others are interested doesn’t make it a good investment; and vice versa if there is little competition (though ask yourself why?).

(2) Funding Method

(a) Initial Deposit

If this is being funded through short term (bridging or equivalent) finance then this will be costly so a refinance will be essential.

If this is funded through your cash savings then many Landlords forget to include the opportunity cost of that money, i.e. the money lost by not using it elsewhere. This should be included when measuring performance.

(b) Initial Purchase

Mortgage costs will make a big difference to your yield. Remember to include transactions costs here, including some high lender fees so don’t just look at the interest rate. The right advice here can be invaluable as can a regular review.

(c) Refinance Cost

It is not only the initial purchase mortgage costs that are key but regular reviews of your finances will allow the correct appropriation of capital to maximise your investment. Refinance to take advantage of better deals, extract equity or to mitigate risk by fixing rates.

(3) Ongoing Cost

(a) Insurance

Buildings insurance is a must but Rent Guarantee may also be essential depending on your strategy. Review these costs with a specialist broker each year to keep your costs down and to make sure you have appropriate cover. Brilliant Money specialise in this field.

(b) Tenant Finding

Needs to be quick on some strategies so many use a Lettings Agent but then you are looking at a significant proportion of income being withdrawn and a big drop in your yield.

A WORD ON COSTS

It is all too easy to say minimise costs. Have a look at what your risks and objectives are. If you are cash poor it may well be worthwhile insuring heavily against non-payment and against Boiler failure etc. Better to pay a small price now than a possibly crippling blow later on.

(c) Property Management

If you do this yourself your yield will be far greater. Using an agent will definitely affect your yield and ability to generate income but make sure you have the time and expertise.

(d) Maintenance & Upkeep

It pays to know a good tradesman or 2 but make the wrong choice and it can be costly.

(e) Regulatory Requirements

These include Gas Safety; EPC’s; furniture requirements; safety obligations; HMO requirements (see HMO Guide on this area – call for details) and many other obligations.

Be aware of your options in these areas and of your approximate costs in these areas BEFORE any investment.

(4) Cost of Exit

Don’t forget that transactions costs apply on sale as well as purchase. These need to be taken into account when looking at your proposed strategy, particularly if you intend to have a high turnover of property.

(a) Tax

Income tax and capital gains tax are areas all too often forgotten by landlords until it is too late. Your personal situation will be unique but make sure you account for these issues or seek professional advice to minimise the impact in the future. Again, your selected strategy will have a huge impact on your preferred tactics in this field.

(b) Cost of Sale

There will be significant transactions costs on the sale. These can vary but are frequently approximated as 2-2.5% of the sale price.

(c) Demand for Property

If you intend to sell, make sure there’s a competitive market to sell to or the value you have on your property may not be where you think it should be.